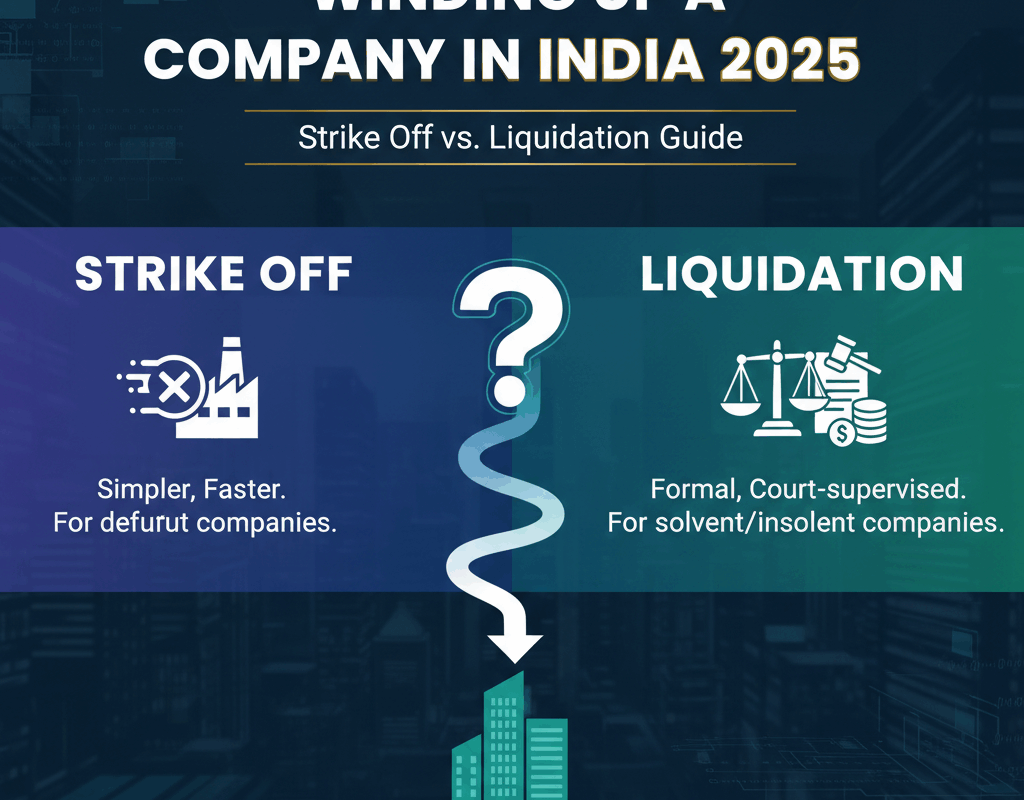

Navigating the legalities of closing a company in India can be complex. Whether you’re considering a fast-track Strike Off for a defunct entity under the Companies Act, 2013, or a formal Voluntary Liquidation for a solvent business under the IBC, 2016, understanding the correct procedure is critical to avoid future liabilities.

This definitive 2025 guide provides a step-by-step comparison of both dissolution methods, complete with an interactive cost calculator, a director’s liability checklist, and expert insights to help you make an informed decision for a clean and compliant corporate closure.

A Definitive Legal Guide to Corporate Dissolution in India

Procedures, Strategies, and Liabilities for Striking Off or Winding Up a Company.

Last Updated: September 2025

Strategic Overview of Corporate Dissolution

The closure of a company in India is a formal, regulated legal process, not merely a cessation of business. Navigating this framework is crucial to protect stakeholders and avoid future liabilities for directors. The process is primarily governed by the Companies Act, 2013 (for 'Striking Off' defunct companies) and the Insolvency and Bankruptcy Code (IBC), 2016 (for 'Voluntary Liquidation' of solvent companies).

Which Path to Choose? An Interactive Pathfinder

Answer three simple questions to determine the most appropriate closure method for your company.

Infographic: Two Paths to Corporate Closure

Striking Off

(Under Companies Act, 2013)

An administrative, fast-track exit for defunct companies with no assets and no liabilities. Simpler, quicker, and less expensive.

Voluntary Liquidation

(Under IBC, 2016)

A formal, comprehensive process for solvent companies with assets and liabilities that require systematic settlement and distribution.

Method I: Striking Off (The Expedited Route)

Governed by Section 248 of the Companies Act, 2013, this is an administrative process overseen by the Registrar of Companies (ROC) and the central C-PACE authority. It's designed for defunct companies to achieve a clean exit efficiently.

Eligibility Gauntlet: Can You Apply?

- Company has not commenced business within one year of incorporation OR has been inactive for the last two financial years.

- Crucially: All liabilities have been extinguished. The company must have NIL assets and NIL liabilities.

- All overdue statutory filings (AOC-4, MGT-7) are complete.

- All company bank accounts are formally closed.

- No pending litigation, inspection, or investigation against the company.

Procedural Roadmap: A Step-by-Step Infographic

Board Meeting

Directors pass a resolution to approve the strike-off and call for a shareholder meeting (EGM).

Shareholder Approval

A Special Resolution is passed by a 75% majority of shareholders to approve the strike-off.

File e-Forms

File Form MGT-14 (for the special resolution) and then the main application Form STK-2 with C-PACE, along with all required documents and a fee of INR 10,000.

Public Notice & Scrutiny

ROC issues a public notice (Form STK-5) inviting objections for 30 days.

Final Dissolution

If no valid objections are received, the ROC strikes off the company's name and publishes a final notice (Form STK-7). The company is officially dissolved.

`Suo Motu` Strike Off by ROC

It's important to note that the ROC can also initiate a strike-off on its own (`suo motu`) if it has reasonable cause to believe a company is defunct. The primary trigger for this is the continuous failure to file annual returns (AOC-4 and MGT-7) for two or more consecutive years. In such cases, the ROC sends a notice to the company and its directors, and if no response is received, proceeds with the strike-off. While this seems like a passive way to close a company, it is highly discouraged as it can lead to director disqualification and other penalties.

Consequences and Revival Provisions

While Strike Off dissolves the company, it's not an irreversible finality. Stakeholders should be aware of two key aspects:

- Continuing Director Liability: The liability of every director, manager, or other officer continues and may be enforced as if the company had not been dissolved. Any fraud or wilful misconduct is not absolved.

- Revival of Company: Any person aggrieved by the strike-off order (e.g., a previously unknown creditor) can file an appeal with the NCLT for revival of the company within 3 years. The ROC can also initiate revival within 20 years if it discovers the company was active or had assets at the time of strike-off.

Method II: Voluntary Liquidation (The Formal Winding-Up)

For solvent companies with assets and liabilities, Voluntary Liquidation under Section 59 of the IBC is the legally mandated route. This is a formal, NCLT-supervised process managed by a licensed Insolvency Professional (IP) as the Liquidator.

The Cornerstone: Declaration of Solvency

Before starting, a majority of directors must make a sworn affidavit declaring that:

- The company has no debt OR can pay all debts in full from the sale of its assets.

- The liquidation is not intended to defraud any person.

Warning: A false declaration carries significant personal liability and penalties for the directors.

Procedural Roadmap: A Step-by-Step Infographic

Shareholder Approval & IP Appointment

Shareholders pass a Special Resolution (75% majority) to approve liquidation and appoint an Insolvency Professional as the Liquidator.

Creditor Approval (If any debts)

Creditors representing two-thirds (2/3rd) of the debt value must approve the resolution within 7 days.

Public Announcement & Claims

Liquidator makes a public announcement inviting all stakeholders to submit their claims within 30 days.

Liquidation Process

Liquidator takes control of the company, sells assets, verifies claims, and distributes proceeds according to the priority waterfall in Section 53 of the IBC.

Final Dissolution by NCLT

Liquidator submits a Final Report to the National Company Law Tribunal (NCLT), which then passes a final Dissolution Order.

The Waterfall Mechanism (Section 53, IBC)

A core element of liquidation is the legally mandated order of payment. The Liquidator must distribute proceeds from asset sales strictly in this sequence. Any remaining surplus is distributed to shareholders.

Liquidation & Insolvency Costs

Fees of the IP and costs of the liquidation process.

Workmen's Dues & Secured Creditors

Wages of workmen for the past 24 months, alongside debts owed to secured creditors who have relinquished their security.

Employee Wages

Salaries and dues of employees (other than workmen) for the past 12 months.

Unsecured Financial Creditors

Loans from banks and financial institutions not backed by collateral.

Government Dues & Remaining Secured Creditors

Statutory dues (e.g., taxes) and debts to secured creditors who enforced their security but had a shortfall.

Any Remaining Debts and Dues

Includes operational creditors and any other outstanding liabilities.

Comparative Analysis: Selecting Your Strategy

The choice between Strike Off and Voluntary Liquidation is a strategic trade-off between speed/cost and legal finality. This comparison will help you decide.

Interactive Chart: Key Differences at a Glance

Strike Off vs. Liquidation: A Comparison

Detailed Comparison Table

| Parameter | Strike Off (Companies Act) | Voluntary Liquidation (IBC) |

|---|---|---|

| Suitable For | Defunct companies with NIL assets and liabilities. | Solvent companies with assets and liabilities to be settled. |

| Authority | ROC / C-PACE (Administrative) | NCLT (Quasi-Judicial) |

| Average Time | 60–90 days (with C-PACE) | 9–12 months or longer |

| Cost | Low (INR 10k fee + professional fees) | High (Liquidator, legal, valuation fees) |

| Complexity | Simple (Director-driven, form-based) | Complex (IP-managed, legal process) |

| Legal Finality | Less conclusive. Can be revived within 3 years. Director liabilities continue. | Highly conclusive. Ends with a final NCLT order, extinguishing claims. |

Cost Estimation Calculator

Get a ballpark figure for the costs associated with closing your company. Please note these are industry-standard estimates and actual costs may vary based on the complexity of the case and the professionals engaged.

Estimated Costs

The Professional's Role in Corporate Dissolution

While directors drive the decision-making, the technical and legal complexities of dissolution necessitate the involvement of qualified professionals to ensure compliance and mitigate risks.

Company Secretary (CS)

The Compliance Expert

Crucial for both processes. A practicing CS ensures all resolutions are correctly drafted, forms (STK-2, MGT-14) are accurately filed, and all procedural requirements under the Companies Act are met. Their certification on forms is often mandatory.

Chartered Accountant (CA)

The Financial Guardian

Essential for preparing the statement of accounts for Form STK-2, confirming nil assets and liabilities. In liquidation, they play a key role in auditing the company's financials for the Declaration of Solvency and managing final tax filings.

Insolvency Professional (IP)

The Liquidator

Mandatory and central to Voluntary Liquidation under the IBC. Appointed as the Liquidator, the IP takes full control of the company, manages the entire process of asset sale, claim verification, and distribution, and liaises with the NCLT.

Director's Liability: A Post-Closure Reality Check

Dissolution of a company does not automatically grant immunity to its directors. The law makes a clear distinction between the corporate entity and the individuals who managed it, especially concerning statutory duties and fraudulent acts.

Liability in a Struck-Off Company

The primary risk post-strike off is the discovery of undisclosed liabilities. Since the process relies on director declarations, any misrepresentation can have severe consequences.

- Undisclosed Creditors: If a creditor emerges after dissolution, they can sue the directors personally to recover their dues.

- Statutory Non-compliance: Any unpaid taxes (Income Tax, GST) or unfulfilled regulatory duties remain the personal liability of the 'officer in default'.

- Fraudulent Activity: If fraud is discovered, directors can face severe penalties and prosecution, and the corporate veil offers no protection.

Liability in a Liquidated Company

While liquidation offers greater finality, director liability still exists, particularly for actions taken before the liquidator was appointed.

- False Declaration of Solvency: This is a serious offence under the IBC, leading to imprisonment and fines.

- Preferential Transactions: If directors favoured one creditor over others shortly before liquidation, the NCLT can reverse the transaction and hold directors liable.

- Fraudulent Trading: If directors continued business to defraud creditors when they knew insolvency was imminent, they can be made personally liable for the company's debts.

Tax Implications of Corporate Closure

Winding up a company is a significant event from a tax perspective. Both the company and its shareholders must account for potential tax liabilities arising from the distribution of assets.

For the Company

- Capital Gains Tax: When the company sells its assets during liquidation, any profit or gain from the sale is subject to Capital Gains Tax in the hands of the company. The tax is calculated on the difference between the sale price and the indexed cost of acquisition of the asset.

- GST and Other Indirect Taxes: The company must file a final GST return (Form GSTR-10) within three months from the date of cancellation of registration. All outstanding GST liabilities must be cleared before dissolution.

For the Shareholders

- Deemed Dividend (Section 2(22)(c)): Any distribution of accumulated profits to shareholders upon liquidation is treated as a "deemed dividend" and is taxable in the hands of the shareholders at their applicable slab rates.

- Capital Gains on Share Liquidation: Any money or asset value received by a shareholder over and above the deemed dividend is treated as consideration for the extinguishment of their shares. This can result in a Capital Gains tax liability for the shareholder, calculated as the value received minus the cost of acquiring the shares.

Pro Tip: Proper tax planning before initiating liquidation is crucial to manage and potentially minimize the tax impact on both the company and its shareholders.

Real-World Scenarios: Which Path to Take?

Let's apply the concepts to two common business situations.

Scenario A: The Dormant Startup

"InnovateNext Pvt. Ltd." was incorporated three years ago but never launched its product. It has no employees, no business operations for the past 2.5 years, no loans, and no creditors. The only bank account was closed last year. The directors want a clean, quick exit.

Recommendation: Strike Off

This is a classic case for Strike Off. The company is defunct, has nil assets and liabilities, and is compliant with its past filings. It meets all the eligibility criteria for a fast and low-cost closure via Form STK-2.

Scenario B: The Successful SME

"QualityFabrics Ltd." has been a profitable business for 15 years. The owners are retiring. The company owns a factory (asset), has outstanding bank loans (liability), and raw material suppliers (creditors). It has significant retained earnings and wants to distribute the proceeds to shareholders.

Recommendation: Voluntary Liquidation

Strike Off is not an option due to the presence of assets and liabilities. The only correct legal path is Voluntary Liquidation under the IBC. An IP must be appointed to sell the factory, pay off the bank and suppliers, and then distribute the surplus to shareholders in a legally compliant manner.

Frequently Asked Questions (FAQ)

No. A company cannot be struck off if it has any outstanding liabilities, including statutory dues like income tax, GST, or PF. All such demands must be fully paid, and a No Objection Certificate (NOC) or closure report from the respective department is often required.

Any property or asset of a dissolved company that was not realized or distributed automatically vests with the Central Government. To access it, an application must be made to the NCLT to revive the company, after which the asset can be properly dealt with.

Yes. A Section 8 company cannot be struck off directly. It must first convert into a regular private or public limited company, a process which itself requires extensive approvals. Alternatively, it can undergo voluntary liquidation, where any surplus assets must be transferred to another Section 8 company with similar objectives, not to its members.

Under the Companies Act, books and papers of a dissolved company must be preserved for a period of 8 years from the date of dissolution. In case of liquidation under the IBC, the liquidator is responsible for preserving the records as per the regulations.

Final Checklist for Directors

Before signing any closure application, every director must personally verify the following, keeping in mind their continuing personal liability.