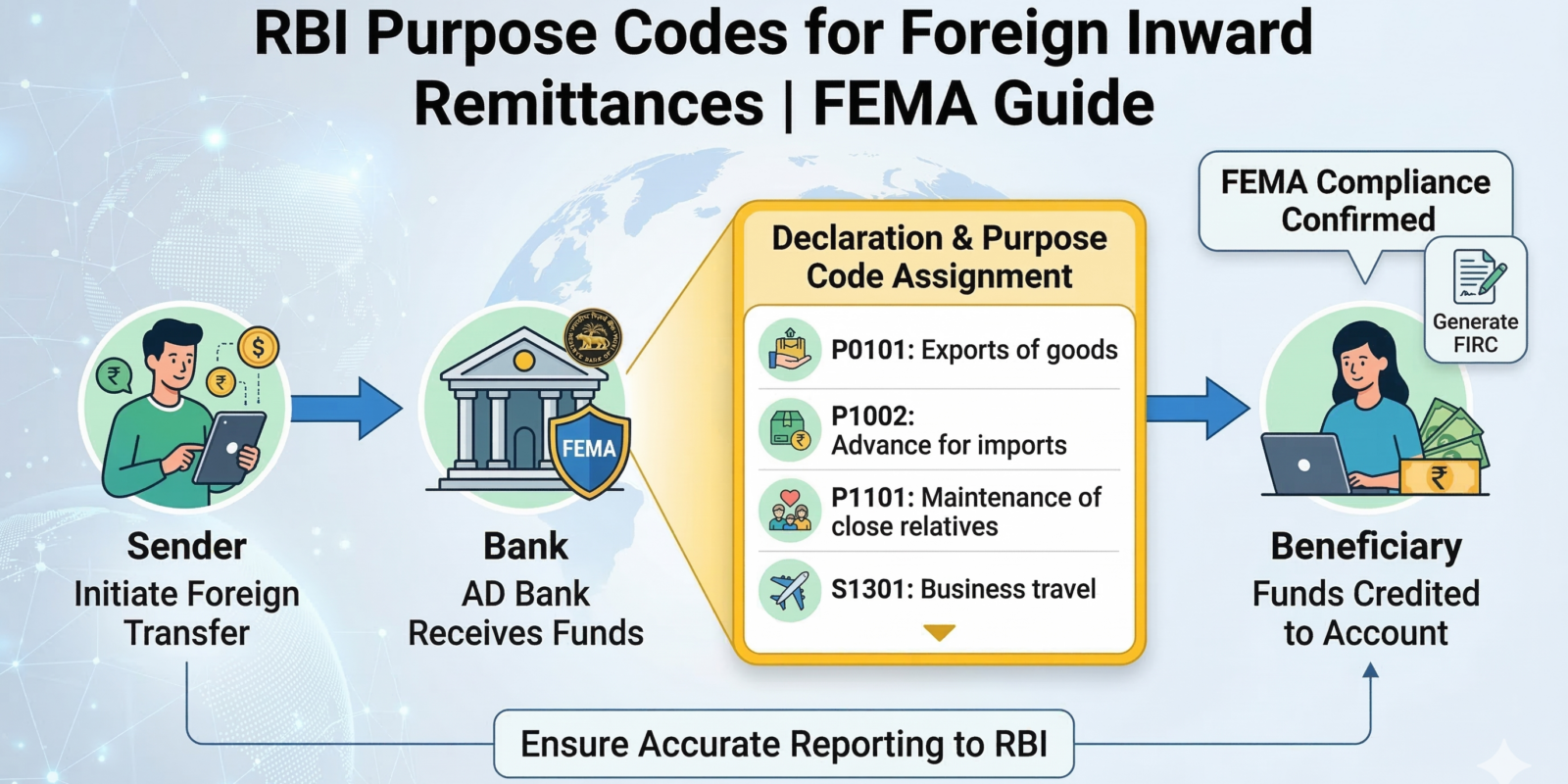

If you work remotely or export digital services from India, your bank likely pauses your foreign inward remittances to ask for an RBI purpose code. This repeated inquiry is not a banking error.

It is a strict statutory requirement under the Foreign Exchange Management Act (FEMA). To clear your funds, you must provide the exact alphanumeric classification, such as P0802 for IT services or P1006 for consulting, along with matching commercial documents.

This guide explains the mechanics of the RBI purpose code system, SWIFT network routing instructions, and the e-FIRC documentation required to satisfy your Authorised Dealer bank and domestic tax authorities.

Regulatory Mechanics of Foreign Inward Remittances

Decoding Purpose Codes, Compliance Protocols, and Taxation Alignment for remote workers and service exporters.

Executive Summary (TL;DR)

- › Your bank asks for a purpose code every time because RBI rules require each foreign credit to be classified and reported by the Authorised Dealer bank under FEMA.

- › The purpose code is the official RBI tag for the reason of the transfer. Payments into India use P codes. Outward payments use S codes.

- › If you do not give the correct code and documents, the bank keeps the remittance pending and asks for an invoice or other proof. In the worst case scenario, they return the payment to its source.

- › Use the correct codes: P0802 for IT services, P1006 for marketing services, P1401 for salary, P1301 for family support, P1302 for gifts. Do not mark commercial client payments as gifts.

- › Speed tip: Ask the sender to mention the purpose code in SWIFT field 70 or 72, or ask your bank to set a standing instruction for regular payments.

The remote digital workforce and commercial service exporters receive regular foreign remittances. Receiving these funds requires mandatory inquiries from the receiving banking institution. Beneficiaries must submit purpose codes and supporting commercial documentation. This is a statutory requirement dictated by the central banking authority.

This report provides a technical analysis of the rules governing foreign inward remittances in India. It explains the Foreign Exchange Management Act (FEMA), Reserve Bank of India (RBI) purpose codes, SWIFT messaging protocols, and domestic tax liabilities.

The Recurring Compliance Loop

Scenario: You receive money from abroad. Your bank asks for a purpose code. You reply and submit the documents. Next month, the exact same process happens again. You wonder why you are stuck in this loop.

The bank is not forgetting your previous declarations. The bank is strictly following RBI reporting rules for each individual foreign credit. Every distinct transaction requires its own documented justification to clear regulatory hurdles.

FEMA and Authorized Dealers

The Foreign Exchange Management Act governs foreign exchange transactions in India. FEMA categorizes transactions into capital account transactions and current account transactions. Payments for foreign trade, freelance service exports, and living expenses are current account transactions.

The RBI delegates foreign exchange monitoring to Authorized Dealer (AD) Category-I banks. These include major institutions like State Bank of India, HDFC Bank, ICICI Bank, and Axis Bank. When an inward remittance arrives, the AD bank must establish the economic reason for the inflow before crediting the domestic account. This fulfills the bank’s duty to report transactions to the RBI.

The RBI Purpose Code System

A purpose code is an alphanumeric tag assigned to a transaction. It classifies the exact economic reason for capital movement. Transactions moving outward use codes starting with S. Transactions moving inward use codes starting with P.

Search RBI Purpose Codes

| Code | Category | Application |

|---|---|---|

| P0006 | Capital Account | Foreign Direct Investment by overseas Investors in equity shares. |

| P0101 | Exports (Goods) | Value of export bills negotiated. Represents physical goods trade. |

| P0802 | IT Services | Software consultancy other than SOFTEX. Used for independent IT contractors. |

| P0807 | IT Services | Off-site Software Exports. Requires formal SOFTEX form compliance. |

| P1006 | Business Services | Business and management consultancy. General advisory and strategy. |

| P1301 | Secondary Income | Family maintenance and savings. Used for personal remittance support. |

| P1302 | Secondary Income | Personal gifts and donations. Non-commercial personal capital transfers. |

| P1401 | Income | Compensation of employees. Used for formal salary from a foreign entity. |

Categorization Framework for Remote Workers

The correct purpose code depends entirely on the nature of the transaction. It does not depend on your formal job title. You must separate commercial income from personal capital transfers.

Commercial Contractor Income

Use this category when you raise invoices for your services.

- ›P0802: Use for software consultancy and implementation support. Do not use this if you deliver a physical software product.

- ›P1006: Use for marketing and general business advisory services.

Personal Capital Transfers

Use this category when the money is strictly personal and not linked to any commercial work.

- ›P1301: Use for family maintenance and savings.

- ›P1302: Use for personal gifts. A business entity cannot send a personal gift.

Macroeconomic Surveillance

The purpose code feeds data into India’s Balance of Payments statistics. The government tracks the volume and origin of foreign capital. This data helps evaluate exchange rate stability and formulate fiscal policies.

Compliance Checks and Fraud Control Triggers

Banks must strictly match the payment details with your declared profile and submitted documents. A mismatch instantly triggers a manual compliance review by the banking authority.

The Mismatch Trigger

A software developer who selects a physical goods export code creates an immediate mismatch. The bank asks detailed questions. The credit moves to an internal review queue. The beneficiary faces delayed access to funds.

The Alignment Path

A remote developer receiving funds under P0802 uploads a matching service invoice. The bank system validates the text and sender profile. The transaction clears the check without human intervention.

When you do not give a code, the bank does not close the inward remittance record. The bank asks for the purpose code and supporting papers. It keeps the remittance pending until it receives the documents required for its FEMA checks. If the bank is not satisfied with the reply, the payment is returned to the source.

The FETERS Reporting Infrastructure

The purpose code you submit does not stay at your local bank branch. The Authorized Dealer bank uploads your transaction details into the Foreign Exchange Transactions Electronic Reporting System. The central banking authority operates this system to track all capital movements.

Every inward remittance, along with its assigned code, enters this national database. This creates a permanent digital footprint of your foreign income. Tax authorities cross-reference this database during assessments. This makes consistency between your bank declarations and your tax filings mandatory.

Suspense Accounts and Return Protocols

When foreign currency reaches an Indian correspondent bank without a valid purpose code, the funds do not enter your personal savings or current account. The bank holds the capital in a temporary suspense account. This is a holding area used until compliance checks conclude.

Banks operate on strict timelines for resolution. The beneficiary usually has a brief window to submit the missing purpose code and the corresponding commercial invoice. If the beneficiary fails to provide acceptable documentation within this compliance period, the bank initiates a return protocol. The funds are reversed and sent back to the originating overseas source. This causes extreme payment delays and damages client relationships.

SWIFT Network Mechanics

Cross-border wire transfers rely on the SWIFT network. The originating bank transmits an MT103 message to the Indian correspondent bank. This message includes narrative fields designed for regulatory data.

Field 70 and Field 72 transmit compliance information. Instruct the overseas sender to embed the RBI purpose code directly into these fields. Automated systems can then parse the data and process the transaction without manual queries.

SWIFT Instruction Template

Provide this text to your foreign client

/PURP/CODE/P0802/Software Consulting

INV Number: [Insert Invoice Number]

Standing Disposal Instructions

Beneficiaries receiving recurring payments can utilize a Standing Disposal Instruction with their bank. An instruction is a formal authorization that allows the bank to apply a pre-defined RBI purpose code to future inward remittances from a specific remitter. This reduces repeated emails and reduces hold time.

- 01. State Bank of India: Provides an automated digital pathway through its Internet Banking portal under the NRI Services module.

- 02. HDFC Bank: Offers Smart Standing Instructions via NetBanking. Users digitally assign the recurring purpose code.

- 03. ICICI Bank: Allows corporate entities to establish standing mandates through Corporate Internet Banking.

Mandatory Document Matrix

Your bank asks for specific documents that match your selected purpose code. Mismatched documents stall the credit process.

| Transaction Type | Primary Code | Required Bank Documents |

|---|---|---|

| Contractor Work | P0802 / P1006 | Commercial invoice. The bank might also ask for the master service agreement or contract. |

| Formal Employment | P1401 | Employment contract and the monthly payslip matching the remittance value. |

| Personal Gift | P1302 | Sender details. The bank asks for relationship proof in specific compliance cases. |

Goods Export versus Service Export Discrepancies

Many remote workers cause compliance failures by selecting incorrect transaction categories. A physical goods export requires entirely different documentation compared to a digital service export.

Physical Goods (P0101)

Selecting this code forces the bank to search government databases for customs shipping bills. If you exported software code instead of physical items, no shipping bill exists. The transaction fails the validation check.

Digital Services (P0802)

Selecting this code tells the bank to expect a commercial invoice for consulting or software development. The bank evaluates the invoice and clears the funds without expecting physical shipping documents.

Audit Retention and The e-FIRC Protocol

As a commercial service provider, the electronic Foreign Inward Remittance Certificate (e-FIRC) or remittance advice is your primary banking document. Your remittance proof from the bank carries the exact purpose code applied to the transaction.

The inward remittance advice issued by the bank supports all future audit and tax documentation. You must extract this document from your bank portal and safely store it in your dedicated tax folders.

Why The Remittance Proof Matters

- ›It proves the realization of convertible foreign exchange in India.

- ›It acts as required evidence for zero-rated GST export claims.

- ›It maps the exact RBI purpose code directly to the specific commercial invoice.

Documentary Evidence and Taxation

Exporting services qualifies for zero-rated Goods and Services Tax. Exporters claiming a refund of unutilized Input Tax Credit must submit the remittance proof from the bank to validate the receipt of foreign exchange.

The purpose code must align with the Income Tax return. Purpose code is a banking classification tag. Income tax head depends on your contract facts. Employee income goes under Salary. Invoice based work goes under Business or Profession. Your tax filing must match your facts and your bank trail.

Tax Head Alignment vs. Banking Classification

The purpose code does not determine your income tax head. The purpose code is strictly a banking classification tag for the RBI.

Your income tax head depends on the factual nature of your contract.

- Employee income goes under the Salary tax head.

- Invoice based independent work goes under the Business or Profession tax head.

Your tax filing must match your contract facts and your bank audit trail.

Case Study: Rohit’s Remittance Strategy

Rohit sits in Pune. He does software development for a United States startup and sends an invoice. The startup sends foreign currency to Rohit’s Indian bank. The bank asks for a purpose code.

Rohit selects P0802 and uploads the invoice. The bank completes its record.

Next month, Rohit’s cousin sends money for his parents’ expenses. Rohit selects P1301 for that specific credit. Rohit keeps the two receipt types strictly separate to avoid commingling commercial revenue with personal maintenance funds.

Standard Operating Process

To maintain clean financial records and avoid regulatory friction, fix a standard process for every incoming foreign transaction.

Do THIS for every foreign credit:

Keep the specific invoice or contract ready before the funds arrive.

Pick a purpose code that perfectly matches the work detailed on that invoice.

Use the identical code pattern each time for the same type of service delivery.

Store the final bank remittance proof alongside the original invoice for future tax and GST assessments.