The Indian tax framework dictates how property owners report rental income and tenants process rent payments.

Taxpayers choose between the New Tax Regime under Section 115BAC and the Old Tax Regime to determine their eligibility for housing deductions like the House Rent Allowance and home loan interest offsets.

Analysis of Taxation Scenarios for Property Owners and Renters in India

The Indian tax framework for real estate income and rent payments involves specific statutory rules. The Union Budget 2026 and the Draft Income-tax Rules 2026 apply to Financial Year 2025-26 and 2026-27. The tax administration requires digital tracking for financial transactions.

Tax rules depend on the chosen tax regime. India uses a dual tax system. Taxpayers select between the Old Tax Regime and the default New Tax Regime under Section 115BAC.

The Old Regime requires documentation for tax planning. It includes the House Rent Allowance (HRA) exemption and Section 80GG rent deductions. The New Tax Regime removes most housing exemptions. It provides lower tax rates.

The Dual Taxation Framework

The Union Budget 2026 confirmed no modifications to the income tax slabs for FY 2026-27. The rates are identical to FY 2025-26. The New Tax Regime is the default framework. Taxpayers with salary or house property income can opt out and select the Old Regime.

New Tax Regime Slabs

The basic exemption limit is INR 4,00,000. A standard deduction of INR 75,000 applies to salaried individuals. A tax rebate under Section 87A up to INR 60,000 applies if total income does not exceed INR 12,00,000.

| Income Bracket (New Regime) | Tax Rate |

|---|---|

| Up to INR 4,00,000 | Nil |

| INR 4,00,001 to INR 8,00,000 | 5% |

| INR 8,00,001 to INR 12,00,000 | 10% |

| INR 12,00,001 to INR 16,00,000 | 15% |

| INR 16,00,001 to INR 20,00,000 | 20% |

| INR 20,00,001 to INR 24,00,000 | 25% |

| Above INR 24,00,000 | 30% |

Old Tax Regime Slabs (Under 60 Years)

The Old Regime permits housing deductions. The basic exemption limit is INR 2,50,000. A standard deduction of INR 50,000 applies to salary income.

| Income Bracket (Old Regime) | Tax Rate |

|---|---|

| Up to INR 2,50,000 | Nil |

| INR 2,50,001 to INR 5,00,000 | 5% |

| INR 5,00,001 to INR 10,00,000 | 20% |

| Above INR 10,00,000 | 30% |

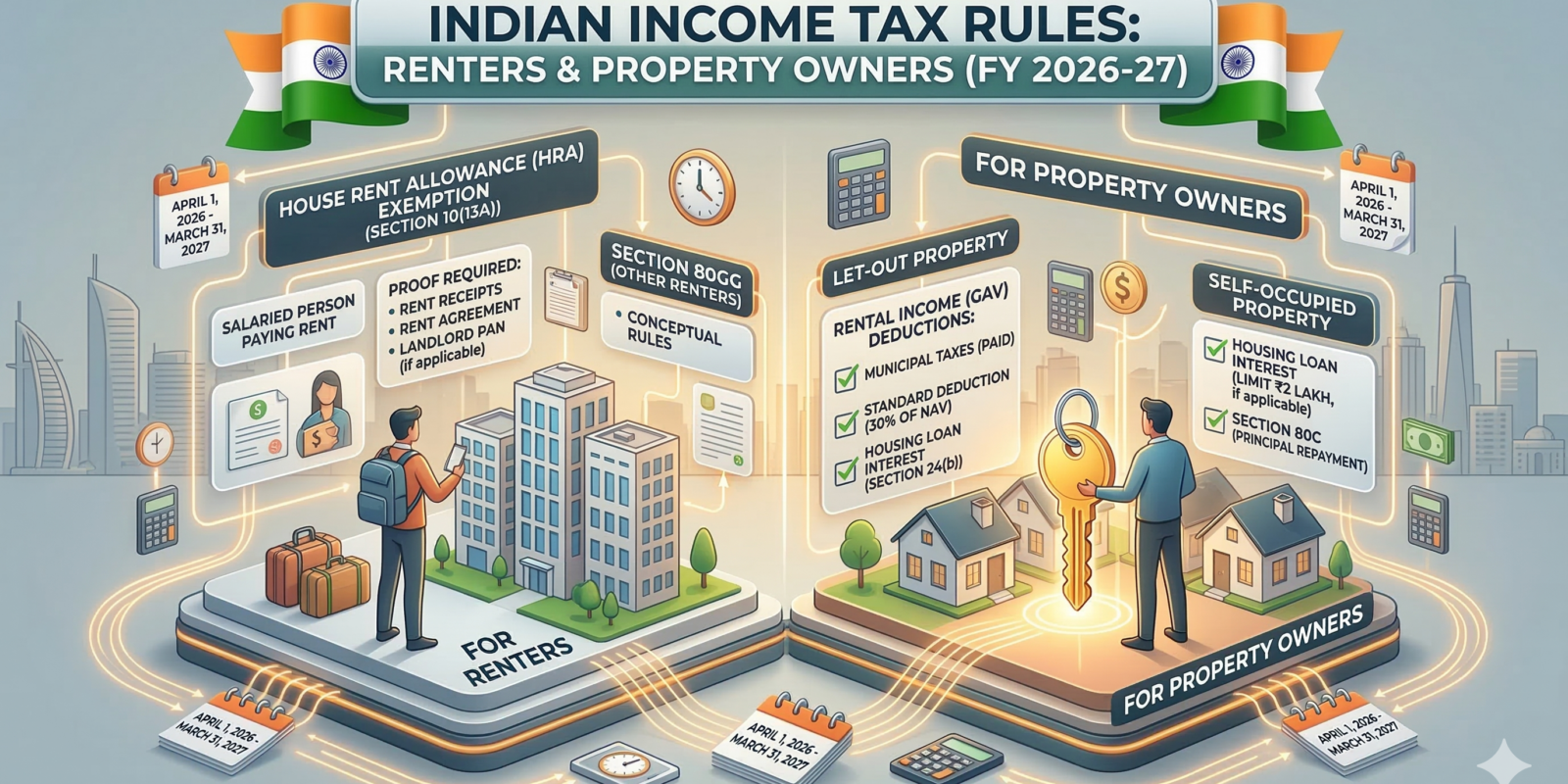

Tax Rules for Renters

Section 10(13A) governs the House Rent Allowance. The exemption requires calculating three limits. The lowest amount is tax-free.

- Actual HRA received.

- Actual rent paid minus 10% of baseline salary.

- 50% of baseline salary for specific cities or 40% for other locations.

The Draft Income-tax Rules 2026 expand the 50% limit. Effective April 1, 2026, renters in Bengaluru, Hyderabad, Pune, and Ahmedabad qualify for the 50% exemption ceiling. This requires remaining in the Old Tax Regime.

Form 124 replaces Form 12BB. Tenants must disclose their exact relationship with the landlord. The tax department cross-references the tenant’s Form 124 with the landlord’s PAN to ensure exact revenue matching.

Section 80GG Deductions

Taxpayers without an HRA component can use Section 80GG. The maximum deduction is INR 5,000 per month. The taxpayer must file Form 10BA electronically.

Withholding Tax (TDS) on Rent

Section 194-IB mandates that individuals paying rent above INR 50,000 per month must deduct tax. The tenant uses their PAN. No TAN is required.

- The standard TDS rate is 2% if the landlord provides a valid PAN.

- If the landlord does not provide a PAN, the TDS rate is 20%. The maximum deduction is capped at the final month’s rent amount.

- The tenant deducts the aggregate annual TDS in March or the final month of tenancy.

- The tenant remits the tax using Form 26QC and issues Form 16C to the landlord.

Tax Computations for Property Owners

Rental income is taxed under Income from House Property. The calculation uses standardized steps.

Gross Annual Value (GAV) compares expected rent against actual rent. The higher figure is selected. Municipal taxes paid by the owner are subtracted to determine the Net Annual Value (NAV).

Section 24(a) provides a flat 30% standard deduction on the NAV. Section 24(b) permits a deduction for home loan interest.

Under the Old Tax Regime, owners of let-out properties can deduct the full interest amount. If this creates a loss, up to INR 2,00,000 can be set off against other income in the current year. Unabsorbed losses are carried forward for eight years. Under the New Tax Regime, loss set-off is completely prohibited. Interest deductions are limited to the extent of the taxable rental income.

Rental Scenarios & Fiscal Outcomes

Select a monthly rent threshold to view the compliance requirements and tax logic.

Annual Rent: INR 3,60,000

Rent is below the INR 50,000 limit. Section 194-IB does not apply. No TDS deduction is required. HRA exemptions depend on salary structure. Section 80GG provides a maximum deduction of INR 60,000 annually.

Gross Annual Value is INR 3,60,000. The landlord deducts municipal taxes. The 30% standard deduction applies. Income is declared via the annual tax return. No TDS credit will appear in Form 26AS.

Annual Rent: INR 7,20,000

Rent exceeds INR 50,000. Section 194-IB applies. Tenant must deduct 2% TDS (INR 14,400) in March. Tenant files Form 26QC. If no landlord PAN is provided, TDS is 20%, capped at INR 60,000.

Gross Annual Value is INR 7,20,000. The TDS deducted by the tenant generates a pre-paid tax credit in the Annual Information Statement (AIS). The 30% standard deduction shields INR 2,16,000 (pre-municipal tax).

Annual Rent: INR 18,00,000

High rent dictates significant TDS obligations. 2% annual TDS equals INR 36,000 withheld in March. The tenant maximizes HRA under the Old Regime to offset high salary taxation.

Property likely carries a large mortgage. Under the Old Regime, full loan interest is deducted. Loss up to INR 2,00,000 offsets salary income. Under the New Regime, loss set-off is blocked entirely.

Evaakil Real Estate Tax Calculator

Statutory Document Templates

The revised Form 124 requires specific fields. Use this structure for HR submission.

Name of Tenant: [Full Name]

PAN of Tenant: [PAN String]

Total Rent Paid (FY): INR [Amount]

Address of Rented Property: [Full Address]

Name of Landlord: [Full Name]

PAN of Landlord: [PAN String]

Relationship with Landlord: [Select: None, Parent, Spouse, Sibling, Other Relative]

Declaration: I certify the rent has been transferred via electronic banking.

Ensure your lease contains these parameters to satisfy tax audits.

- Clear statement of monthly rent amount.

- Clause specifying who pays municipal taxes.

- Mandatory inclusion of both tenant and landlord PAN.

- Clause allowing tenant to deduct TDS under Section 194-IB if applicable.

Frequently Asked Questions

No. Section 115BAC eliminates the deduction for interest on borrowed capital for self-occupied properties. For let-out properties, the interest deduction is limited strictly to the rental income generated. It cannot create a loss to set off against other income.

You become an assessee in default. The penalty includes 1% interest per month for delayed deduction. Late filing of Form 26QC incurs a fee of INR 200 per day.

Tax authorities scrutinize cash payments. It is highly recommended to transfer rent via banking channels to maintain an audit trail. Form 124 processing flags high cash declarations.