Losing a job is difficult enough without facing unexpected tax bills on your final settlement. In India, the tax treatment of corporate severance pay differs sharply from statutory retrenchment compensation.

While standard severance is fully taxed as profits in lieu of salary under Section 17(3)(i), specific exemptions exist under Section 10(10B) of the Income Tax Act. Qualifying for this tax relief requires meeting the strict “workman” criteria established by the Industrial Disputes Act of 1947.

This guide details the tripartite calculation mechanism, the INR 5,00,000 statutory exemption limit, and the step-by-step process for filing Form 10E to claim Section 89(1) relief.

The following sections clarify exactly how the income tax department views notice pay recoveries, ESOP vesting, and the legal distinction between a forced termination and a voluntary resignation.

Severance Pay Tax Validation in India

A precise validation of exemption frameworks under Section 10(10B) and the Industrial Disputes Act of 1947.

Validation of the Analytical Query

The premise regarding severance tax exemption is correct. However, it requires a statutory correction. The exact provision within the Income Tax Act of 1961 is Section 10(10B), rather than Section 10(10)(b). There is no Section 10(10)(b) for retrenchment. Section 10(10) governs Gratuity payouts exclusively.

The calculation parameters related to the 15 days of average pay based on the preceding three months for every completed year of service are completely accurate. They reflect the rules established by the Industrial Disputes Act of 1947.

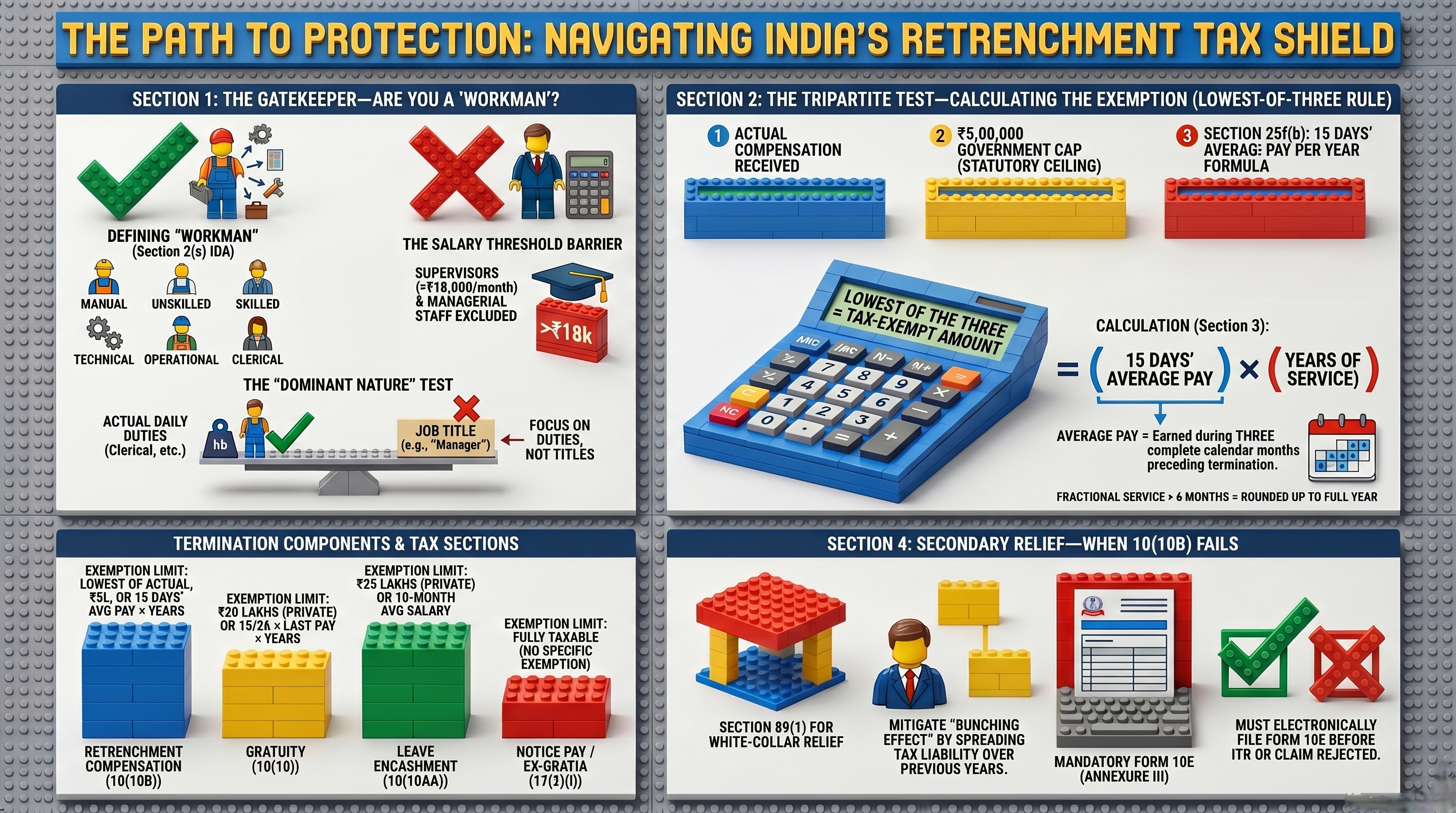

Visual Summary of Payouts

The infographic above outlines the structural flow of severance packages and retrenchment compensation across different employment scenarios in India. It clearly maps the boundaries between taxable and exempt components during a full and final settlement.

Severance vs. Retrenchment

Tax liabilities demand a strict legal boundary between corporate severance pay and statutory retrenchment compensation.

| Category | Nature | Tax Status |

|---|---|---|

| Standard Severance Pay | Contractual obligation or ex-gratia payment based on HR policies. | Fully Taxable under Section 17(3)(i). |

| Retrenchment Compensation | Statutory mandate under Section 25F of the Industrial Disputes Act. | Partially Exempt under Section 10(10B). |

The Tripartite Calculation Mechanism

Section 10(10B) sets a strict limit. The tax-exempt portion is the absolute lowest of three calculated values.

- The Actual Amount: The exact monetary value received from the employer.

- The Government Cap: A fixed limit of INR 5,00,000.

- The Service Formula: 15 days of average pay multiplied by completed years of continuous service.

Average pay is calculated based on wages earned during the three complete calendar months preceding the termination date. Fractional years exceeding six months round up to a full year.

Visual Representation: The exemption is capped at the lowest bar.

The Continuous Service Rule

The Industrial Disputes Act requires a specific duration of employment to trigger retrenchment benefits. An employee must complete one year of continuous service under Section 25B to qualify for the statutory payout calculation.

The law defines one year as 240 days of actual work within the preceding twelve calendar months. Days spent on approved leave, maternity leave, or temporary employer-mandated layoffs count toward this 240-day requirement. If the employment duration falls short of 240 days, the statutory retrenchment compensation clause does not apply, and any severance provided becomes fully taxable.

Component Breakdown of Average Pay

The phrase average pay has a strict legal definition under the framework. It includes the basic salary and the dearness allowance. It explicitly excludes annual bonuses, employer contributions to provident funds, and gratuity payments.

To determine the correct average, you must sum the eligible components from the three complete calendar months immediately preceding the termination date and divide that total by three. This specific average figure feeds directly into the 15 days calculation formula required by Section 10(10B).

Defining the Workman

Section 10(10B) only applies if the employee qualifies as a workman under Section 2(s) of the Industrial Disputes Act. This definition excludes personnel employed in a managerial capacity or those in a supervisory role earning above specific salary thresholds.

The revised salary limit for supervisors under recent labor framework updates stands at INR 18,000 per month. Individuals earning above this amount in supervisory roles lose their workman status and face full taxation on their severance.

The Plight of the IT Sector

Modern service sectors, including software development and digital services, rarely benefit from Section 10(10B). Information Technology professionals usually earn well above the INR 18,000 limit and possess technical autonomy or project management duties. Consequently, their standard severance pay is fully taxable. The lump sum added to the regular yearly salary frequently pushes the individual into the 30 percent tax bracket.

Impact of the Default New Tax Regime

As of the 2026 financial assessments, the New Tax Regime under Section 115BAC operates as the default system for all taxpayers. Employees facing termination must evaluate their tax position carefully. The retrenchment compensation exemption under Section 10(10B) remains available under both the old and new tax regimes. The choice of regime will not eliminate this specific exemption.

However, claiming relief under Section 89(1) for arrears or the taxable portion of severance requires a comparative calculation. Taxpayers must compute their liabilities across the old and new regimes for all applicable past years to determine the exact relief amount. Filing Form 10E is still mandatory regardless of the chosen regime.

Resignation vs. Forced Termination

The method of exit dictates the legal standing of the payout. If an employee submits a resignation letter, even under severe corporate pressure, the exit is legally classified as a voluntary resignation. Voluntary resignations completely invalidate the application of Section 10(10B).

The exemption requires formal, employer-initiated retrenchment. The termination letter must explicitly state that the employment is being severed due to redundancy, role elimination, or company restructuring. Documentation is the only defense during a tax audit. Employees should secure formal layoff notices rather than yielding to requests for voluntary resignation if they intend to claim the tax exemption.

Notice Pay Recovery and Payouts

Notice period dynamics create significant tax confusion during final settlements. When a company decides to terminate an employee immediately and pays the notice period salary in lieu of them working, this amount is fully taxable. It is treated as standard salary income under Section 17(1).

Conversely, if an employee resigns and leaves before serving the full notice period, the company will deduct unserved notice pay from the final settlement. The Income Tax Act currently offers no mechanism to reduce the gross taxable salary by this recovered amount. The employee is taxed on the gross salary earned, suffering a dual financial penalty. Judicial appeals on this matter have largely favored the revenue department.

ESOPs and Equity During Layoffs

Technology companies frequently include accelerated vesting of Employee Stock Ownership Plans during severance. This equity component does not qualify for the Section 10(10B) exemption. The allotment of shares triggers perquisite taxation.

The difference between the Fair Market Value and the exercise price is taxed as salary income in the year of exercise. Employees must separate the cash retrenchment compensation from the equity perquisite when calculating their total tax liability during a layoff.

Non-Compete Clauses in Settlements

Settlement agreements often contain non-compete clauses. Employers pay a specific sum to restrict the departing employee from joining a competitor for a set duration. The tax department classifies non-compete fees arising from an employment relationship as profits in lieu of salary under Section 17(3).

This amount is fully taxable at applicable slab rates. It cannot be merged with the retrenchment compensation to artificially inflate the claim against the INR 5,00,000 exemption limit.

Legal Precedents on Capital Receipts

Courts occasionally distinguish between standard severance and compensation for the right to sue. If an employer pays a settlement specifically to prevent the employee from filing a lawsuit regarding workplace injury or character defamation, legal tribunals sometimes classify this payment as a capital receipt.

Capital receipts fall completely outside the scope of taxable salary. Proving this requires extremely specific legal drafting in the separation agreement. Standard termination letters detailing ex-gratia payments do not meet this threshold.

Cross-Border Employment and NRI Taxation

Employees holding Non-Resident Indian status face different tax mechanisms. If the severance pay accrues due to employment exercised in India, it is taxable in India regardless of the current residential status. Double Taxation Avoidance Agreements might offer relief. Taxpayers must present a Tax Residency Certificate from their current country of residence to claim treaty benefits and avoid dual taxation on the settlement amount.

Intersections with Maternity Leave

Terminating an employee on active maternity leave violates the Maternity Benefit Act. If a settlement is reached, the compensation is heavily scrutinized. The severance component remains subject to Section 10(10B) rules, while maternity benefit payouts are entirely tax-free. Employers must distinctly separate these two components in the full and final settlement to avoid unwarranted tax deductions on the maternity portion.

Insolvency and Bankruptcy Scenarios

When a company faces liquidation under the Insolvency and Bankruptcy Code, employee dues hold a high priority. The resolution professional calculates the retrenchment compensation. The tax treatment remains identical. However, the actual payout might be delayed or prorated based on the liquidation estate. Employees receive Form 16 detailing the TDS only when the resolution professional processes the actual cash disbursement.

PF and Gratuity Separation

Severance packages frequently cause confusion regarding statutory dues. Provident Fund accumulations and Gratuity are entirely separate legal entitlements. Employers cannot bundle Gratuity into a severance offer to make it look larger. Gratuity has its own distinct tax exemption framework under Section 10(10). Employees must ensure their full and final settlement clearly delineates the severance ex-gratia from statutory Gratuity and leave encashment components.

Fixed-Term Contract Rules

The modern corporate sector relies heavily on fixed-term employment contracts. Under Section 2(oo)(bb) of the Industrial Disputes Act, the expiration or non-renewal of a fixed-term contract does not constitute retrenchment. If an employer offers a payout upon the natural expiration of a contract, it is treated as a standard bonus or ex-gratia payment. It is fully taxable and ineligible for the Section 10(10B) exemption.

Agreement Drafting Safeguards

The wording of the separation agreement directly impacts the tax assessment. If an agreement uses terms like “ex-gratia,” “golden parachute,” or “goodwill payment,” the assessing officer will likely tax the entire amount under Section 17(3). To claim the retrenchment exemption, the document must explicitly state that the payment is “retrenchment compensation” provided due to “redundancy” or “role elimination.” Proper legal drafting serves as the primary defense during a tax scrutiny proceeding.

Tax Deduction at Source Mechanics

Employers process severance under Section 192 of the Income Tax Act. Corporate payroll systems default to treating the entire severance package as fully taxable salary. They will deduct TDS accordingly.

Employees must proactively submit legal declarations claiming Workman status and requesting the Section 10(10B) exemption before the final settlement is processed. If the employer refuses to apply the exemption at the source level, the individual faces a heavy initial tax burden and must claim a refund while filing their annual tax return.

Income Tax Return Filing Directives

Taxpayers must report severance pay accurately in their tax returns. The entire gross amount received must appear under the Gross Salary head in Schedule S.

The claimed exemption amount must then be reported under the specific dropdown section designated for Section 10(10B) Retrenchment Compensation. Subtracting the exemption from the gross salary yields the net taxable figure. Taxpayers should retain the full and final settlement letter, the calculation sheet, and bank statements as documentary evidence in case of an assessment query.

Mitigation: Relief Under Section 89(1)

If severance is fully taxable, Section 89(1) of the Income Tax Act provides a procedural method to mitigate the bunching effect of receiving a large sum in a single financial year.

Taxpayers must calculate the tax difference by apportioning the severance across the past years of service. If the current year tax burden exceeds historical apportionment, relief is granted.

Mandatory Requirement: The taxpayer must file Form 10E electronically on the government e-filing portal before submitting their standard Income Tax Return. Failure to file Form 10E results in automatic rejection of the relief claim.

Templates

Below are basic formats related to severance documentation.

Format: Basic Demand for Form 10E Data

To: HR Department / Payroll Team Subject: Request for historical salary data for Form 10E filing Dear Team, Following my recent full and final settlement, I intend to file Form 10E to claim relief under Section 89(1) for the severance component. Please provide a month-wise breakdown of my salary and the exact allocation of the arrears/severance over my tenure. Sincerely, [Your Name]

Frequently Asked Questions

No. Form 10B is an audit report for charitable trusts. Section 10(10B) is the income tax clause for retrenchment compensation exemptions.

No. VRS is governed by Section 10(10C) and requires a scheme formally approved by the Central Board of Direct Taxes. Standard corporate layoffs do not qualify as approved VRS.

Notice pay is considered standard ex-gratia or profits in lieu of salary. It is fully taxable under Section 17(3)(i) and lacks specific exemptions.