Many independent professionals try to lower their tax liability by directing foreign client payments into the bank accounts of non-working spouses or parents. Tax authorities classify this as an illegal application of income.

The Central Board of Direct Taxes actively uses data analytics to match foreign inward remittances with individual PAN records. If your foreign exchange receipt does not align with your registered service contract, you trigger Section 64 clubbing provisions, lose your zero-rated GST export status, and violate FEMA realization timelines.

This document details the specific statutory mechanisms governing income attribution and how the government detects intra-family income shifting.

Legal and Regulatory Architecture Governing Income Attribution, Foreign Exchange, and Tax Compliance for Indian Freelancers

A factual breakdown of why routing client payments to family bank accounts violates direct tax rules, Goods and Services Tax laws, and foreign exchange mandates.

Filter By Topic

The Jurisprudence of Income Attribution

Independent professionals routinely provide specialized services to international clients. This generates foreign exchange. Many individuals direct these payments into the bank accounts of non-working spouses or parents. The intent is to lower the primary earner tax liability by shifting income to individuals in lower tax brackets.

Tax authorities apply a specific test in these scenarios. They separate the Diversion of Income by Overriding Title from the Application of Income.

Diversion versus Application

Diversion occurs when income goes to a third party due to a legal right or court order before it reaches the taxpayer. In these specific events, the diverted money is not taxable for the original earner because they never possessed a legal right to claim it.

Application of income occurs when a taxpayer receives the right to the income and then voluntarily chooses to direct that money to a family member. Directing a client to pay a spouse constitutes an application of income. The income legally belongs to the freelancer the moment the service finishes. The total amount remains fully taxable in the hands of the freelancer.

| Legal Doctrine | Conceptual Mechanism | Taxability Outcome |

|---|---|---|

| Diversion by Overriding Title | Transfer mandated by a pre-existing legal right or court decree. | Not taxable for the primary taxpayer. Assessed for the recipient. |

| Application of Income | Taxpayer voluntarily directs legally accrued income to a family member. | Fully taxable in the hands of the primary taxpayer. |

Anti-Avoidance Mechanisms

The Income Tax Act contains specific rules to stop intra-family income routing.

Section 64: The Clubbing Provisions

Section 64 mandates the clubbing of shifted income back into the taxable income of the primary earner. A common tactic involves a freelancer paying their spouse a salary and claiming it as a business expense. Section 64(1)(ii) stops this. If a spouse receives a salary from a business where the taxpayer has substantial interest, that money is clubbed with the taxpayer income.

There is one exception. The spouse must possess verifiable technical qualifications. The work must be real. The tax officer will demand documentary evidence of the spouse academic degrees and the actual work produced. Without this proof, the salary is added back to the freelancer income.

Section 44ADA: The Presumptive Taxation Paradox

Section 44ADA provides a simplified tax scheme for specific professionals earning up to 75 lakh Rupees annually. Eligible professionals declare exactly 50 percent of their gross receipts as taxable profit. The law dictates that all business expenses, including employee salaries, are already absorbed within this flat 50 percent deduction.

A professional using Section 44ADA cannot separately deduct any sub-contracting fee paid to a family member. If the tax officer finds out, they will attribute the entire gross receipt back to the primary freelancer. This can push the total receipts above the 75 lakh threshold, invalidating the Section 44ADA benefits entirely.

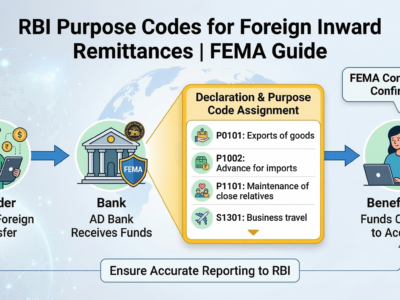

Goods and Services Tax and Foreign Exchange Rules

The Section 2(6) Acid Test for Service Exports

Exporting services is a zero-rated supply under GST. The exporter does not charge IGST and can claim refunds on business expenses. This status depends on five strict conditions under Section 2(6) of the IGST Act.

- The supplier location is in India.

- The recipient location is outside India.

- The place of supply is outside India.

- The payment is received by the supplier in convertible foreign exchange.

- The supplier and recipient are distinct entities.

The fourth condition is absolute. The payment must be received by the registered supplier. If the money goes to the personal domestic bank account of a spouse, this condition fails. The transaction loses its zero-rated status and attracts an 18 percent IGST liability.

FEMA Realization Mandate

The Reserve Bank of India monitors cross border transactions. Service exporters must realize and repatriate proceeds within 15 months from the date of export. When a foreign client pays a spouse directly, the freelancer open export invoice has no matching inward remittance. This creates an absolute default on the 15 month FEMA mandate.

The Surveillance Matrix

The Central Board of Direct Taxes utilizes advanced data analytics to monitor financial transactions. The Annual Information Statement aggregates data from commercial banks and foreign exchange dealers. Every foreign inward remittance maps directly to the Permanent Account Number of the receiving account holder.

When a freelancer shifts payments to a spouse savings account, the automated systems detect the data mismatch. The spouse Annual Information Statement shows high-value foreign remittances categorized under commercial purpose codes. This triggers automated intimations and scrutiny assessments.

ICAI Joint Taxation Proposal (Feb 2026)

The Institute of Chartered Accountants of India proposed an optional joint taxation system for married couples for the Union Budget 2026. This proposal allows couples to voluntarily aggregate their household income and split it equally for tax calculation. If enacted, this policy would legally permit the tax benefits that individuals currently attempt through unlawful income diversion. Until the government passes this law, strict individual assessment remains mandatory.

The Gift Mechanism and Section 64(1)(iv)

Many taxpayers attempt a secondary routing method. They receive the freelance income in their own account and then gift the capital to their spouse. The spouse then invests this money into a Fixed Deposit.

The Income Tax Act anticipates this move. Section 64(1)(iv) applies immediately. When an individual transfers an asset to their spouse without adequate consideration, any income generated from that asset belongs to the transferor. The bank pays interest to the spouse. The tax department clubs that interest back to the original freelancer. You must pay tax on the FD interest at your applicable slab rate.

Foreign Exchange Audit Trails and Compliance

The Reserve Bank of India mandates strict timelines. Exporters must realize and bring export payments to India within six months from the date of the service export. Directing payments to family members shatters the regulatory audit trail.

The FIRC and SOFTEX Disconnect

Banks require clear documentation to issue a Foreign Inward Remittance Certificate. Software and IT service exporters must also file SOFTEX forms to validate their exports. When a spouse receives the money, the bank cannot link the inward remittance to the exporter invoices. This breaks the documentation chain required for GST refunds. The tax department will deny your GST refund application because you lack the FIRC in your registered business name.

The Three Way Agreement Mandate

The RBI permits third party payments for exports only under rigid conditions. The bank demands a formal three way agreement between the foreign client, the exporter, and the third party receiving the funds. The exporter must declare this arrangement in the initial export declaration. Foreign clients rarely agree to sign legal contracts involving an unregistered family member. Without this agreement, the bank views the spouse account receipt as highly suspicious.

Compliant Methods for Tax Reduction

Taxpayers who do not file under the Section 44ADA presumptive scheme have legal options. You can hire your spouse if they possess verifiable skills and manage a legitimate business function.

Section 40A(2) and Fair Market Value

You must sign a formal freelance or employment contract. The remuneration must match the fair market value for those specific skills. Section 40A(2) of the Income Tax Act gives tax officers the power to disallow business expenses if they deem payments to relatives as excessive or unreasonable. If you pay your spouse double the market rate for basic data entry, the officer will disallow the excess amount.

Tax Deducted at Source

You must comply with standard business regulations. This requires deducting Tax Deducted at Source before transferring the payment to your spouse. You must file TDS returns and issue a Form 16 or Form 16A. This creates a valid, verifiable business expense that withstands regulatory scrutiny.

The Direct Invoicing Vulnerability

Many individuals attempt a more aggressive strategy by asking the foreign client to draft the service contract directly in the name of a family member. This represents an amplified version of the standard salary mechanism. While it appears harder to track on the surface, the core vulnerability remains identical.

Execution Decisions and Skill Verification

Tax officers investigate who makes the actual execution decisions. They demand proof of the technical skills required to perform the contracted work. If the family member lacks the specific qualifications needed to write code, design graphics, or consult, the officer will attribute the entire income back to the actual earner. You will then owe tax on the full amount.

Client Contract Compliance Checks

A major practical hurdle exists with this method. Corporate clients enforce strict compliance policies. They require the actual service provider to sign the legal agreements. They rarely agree to execute contracts with an unrelated third party. If the tax department audits your filings, they will demand to see the original client contract. Failing to produce a contract matching the bank recipient triggers immediate penalties and the absolute loss of GST export benefits.

Compliance Risk Assessor Tool

Use this interactive module to evaluate the legal vulnerability of your payment routing structure based on the statutory guidelines discussed above.

Visual Data Mapping

The chart below displays the legal remittance flow versus the flagged non-compliant flow.

Frequently Asked Questions

Standard Contract Clause Templates

If your family member possesses legitimate technical skills and you wish to employ them legally, you must maintain formal documentation. Below is a sample plain text format for a sub-contractor clause.

Date: [Insert Date]

Primary Contractor: [Your Name / Company Name]

Sub-Contractor: [Spouse/Family Member Name]

1. Scope of Services: The Sub-Contractor possesses a degree in [Insert Qualification] and will provide specific technical services including [Insert Exact Tasks].

2. Remuneration: The Primary Contractor will pay a fee of [Insert Amount in INR] per month.

3. Market Valuation: This fee aligns with current market rates for identical services provided by an independent third party.

4. Taxation: The Primary Contractor will deduct Tax Deducted at Source under section 194J of the Income Tax Act before making payment to the Sub-Contractor.

Signatures required below to validate this agreement prior to the commencement of any work.

{kind=link}

{kind=link}